What’s Going On in the Stock Market?

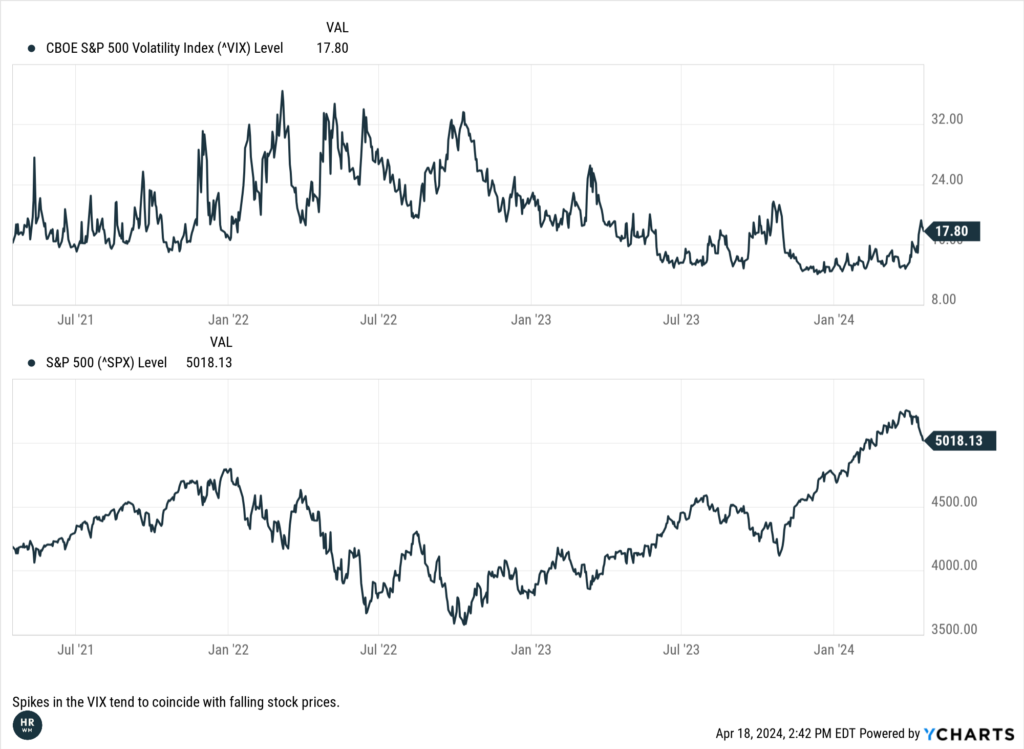

At its peak so far this year, the S&P 500 was up 10.16% on March 28. As of market close on April 19, the S&P had given back roughly half of those gains and closed at 4.14% gains for the year. The Nasdaq peaked at 9.53% gains on April 11 and closed on April 19 at 1.80% gain. That’s a relatively quick reversal and a significant change from the breathless march higher through the first 3 months of the year. Although it isn’t followed as closely by the average investor as the Nasdaq and S&P 500, US Treasury yields are an important indicator of the health of the bond market. The 10 year US Treasury yield started the year at 3.94% and has since climbed to 4.63%. The last time the 10 year yield was at this level and rising was late September of last year. If you’re a long time reader, you most likely recall that bond yields and prices move in opposite directions and that rising bond yields correspond with falling bond prices. Since March 28 we have seen both stock and bond prices fall and it’s not surprising that this negative price action has coincided with an increase in volatility as measured by the CBOE S&P 500 Volatility Index, or the VIX.

CBOE S&P 500 Volatility Index and the S&P 500

Why Is the Stock Market Falling?

Any time we examine price action in a market, explanations will only be partially correct. There are simply too many variables at play to say with absolute confidence that we have the full picture of what moves the markets. However, it’s plausible that several major factors were at play during the recent string of losses. I have heard secondhand that some people believe the market is falling due to inflation, which is partially accurate. The stock and bond markets took a beating in August, September, and October of 2023. By the beginning of 2024, however, the stock market was decidedly in a strong upward trend on several hopes or beliefs. Among those were 1) the assumption that the Federal Reserve had not only finished hiking interest rates, but that they would cut interest rates soon and fast, 2) that corporate earnings would continue to come in strong and there would be no material economic slowdown, and that 3) the geopolitical situation would stabilize or even improve. Throughout the course of the year, that first expectation has been soundly dashed and in recent weeks the third assumption has been challenged. Let’s take a closer look at each and how they have changed throughout the year.

The markets were pricing in six quarter point rate cuts at the beginning of the year. That would mean the Federal Funds rate falling from an upper range of 5.50% to 4.00% by year-end. This type of reduction in interest rates would reduce borrowing costs for individuals and businesses alike. Economic theory suggests that when interest rates are low, money moves more freely, and this tends to allow the economy to grow more rapidly. Individuals can leverage their future income for current purchases using loans and revolving lines of credit at a lower cost and businesses can borrow through the issuance of bonds with less interest maintenance cost and put those funds towards expansion. In short, lower interest rates lead to more money in the system and more money in the system means more growth. However, more money in the system also tends to be an inflationary pressure and therein lies the problem.

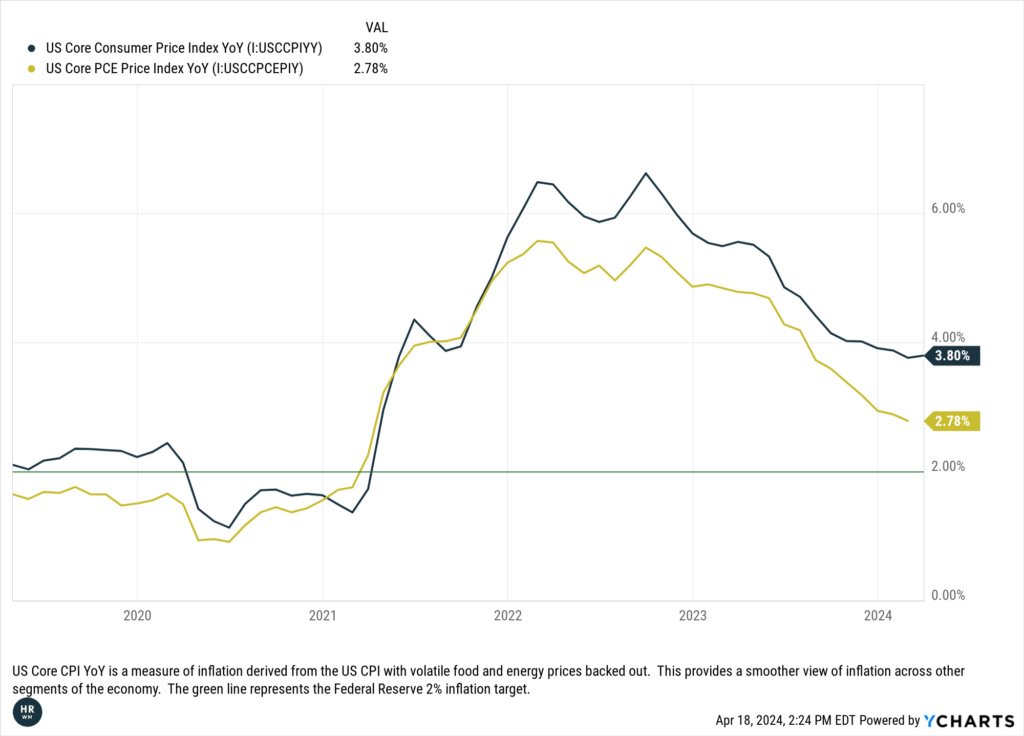

Inflation is a partial explanation of falling stock prices in that the Federal Reserve does not want a rebound in inflation to occur as it did in the 1970s. The Federal Reserve has a dual mandate of price stability (containing inflation) and maximum employment and with headline employment figures like the unemployment rate still strong, the Federal Reserve can remain focused on inflation. It is not the case that inflation has bounced back, but disinflation (slowing of the pace of price inflation) has flatlined in recent months as can be seen in the chart of US Core CPI below. Core PCE, a different measure of inflation that is favored by the Fed, has made more progress towards the 2% target, but the newest data will not be released until Friday the 26th so Core CPI data is the most recent inflation measure the markets can rely on. Stagnating disinflation coupled with strong employment figures means the Fed can reasonably maintain higher interest rates for longer than previously expected to attempt to contain inflation without being overly concerned about a negative impact to employment. In short, don’t expect rate cuts soon unless something changes in the form of continued disinflation (good) or weakening employment (bad). This was something the market was able to ignore through the first three months of the year because the other assumptions mentioned above were still firmly in place. But multiple consecutive data points combined with hawkish messages from Federal Reserve officials changed the market outlook and now Fed Funds futures markets are pricing in only one rate cut by year-end. Recalling the expectation in January of a Fed Funds rate of 4% by year-end, the current expectation of 5.25% by year-end is a substantial change in the outlook for access to “easy money.”

US Core CPI and Core PCE Year-Over-Year

The situation with inflation and Federal Reserve interest rate policy is not occurring in a vacuum. The second assumption mentioned above was that corporate earnings would remain strong and there would be no material economic slowdown. In large part economic growth is still strong. Although there have been some disappointments in the details of a few earnings reports recently, the earnings support largely remains intact and employment figures continue to remain positive. Unfortunately, we may be back in a “good news is bad news” scenario where strong employment data reinforces the Fed’s ability to keep interest rates higher for longer. This is a familiar situation that has ebbed and flowed for over a year now. Strong employment is good for the economy and for workers, but it’s not supportive of interest rate cuts and higher interest rates are viewed as a negative. This leaves strong employment data in a strange quantum state of being both good and bad at the same time.

The third assumption we’re examining is that the geopolitical situation would stabilize or even improve throughout the year. Unfortunately, this has not been the case and it could be argued that the geopolitical tensions in the Middle East have materially deteriorated in recent weeks. This is, of course, concerning for non-financial reasons, but as I have mentioned in the past, the markets are impassive and focus more on the economic impact of geopolitical turmoil. Typically, this means that the market will react to perceived economic outcomes of a conflict such as the effect that might have on commodities. One major commodity in the Middle East is oil and oil prices affect all prices. So, if tensions boil over into open conflict which expands throughout the region and substantial damage is done to oil infrastructure in oil producing nations, then oil prices may increase. If oil prices increase, then transportation becomes more expensive which means shipment of goods becomes more expensive and those goods themselves cost more to the end consumer. In essence, oil prices increasing can be a substantial inflationary pressure. That brings us back to the first point of inflation and rate cut expectations. Upward pressure on inflation is unwelcome news for interest rate expectations. Of course, increasing oil prices aren’t the only concerns of expanding geopolitical conflicts, but it is one example of why recent news may have contributed to falling stock prices.

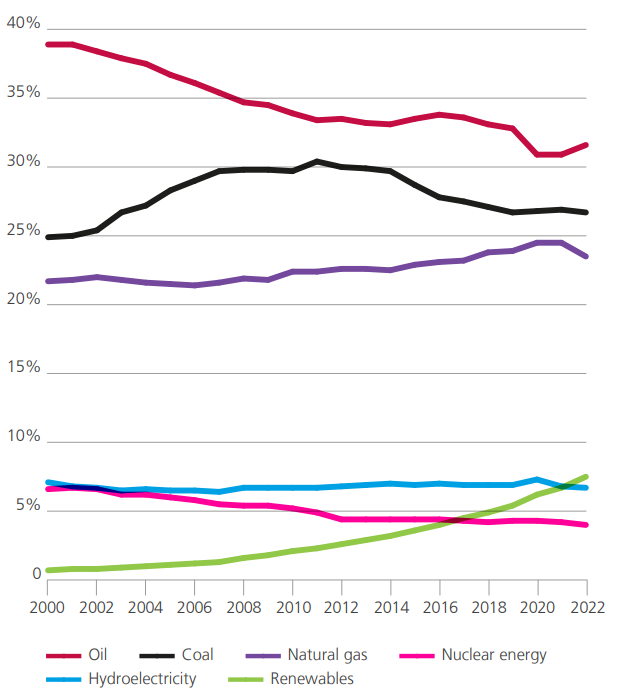

For those interested in better understanding global oil supply and consumption, while the Middle East as a region produces the most oil in the world, the United States is in fact the largest oil producer as a country. According to the Energy Institute Statistical Review of World Energy, in 2022 the United States produced over 17.7 million barrels per day (b/d) or 18.9% of the global oil supply with Saudi Arabia being the second largest producer at 12.9% of the world oil supply. Regionally, the Middle East supplied 32.8% of global oil supply and 26.9% came from North America. The United States also has the greatest demand for oil, consuming over 19 million b/d or approximately 19.7% of global supply. While oil is still the largest source of energy globally, it has been declining as a source of energy and renewables, while still small, are gaining share of global energy source most rapidly of all energy types.

Share of Global Primary Energy

Will the Stock Market Continue to Fall?

No one knows what the market will do tomorrow or next week. It is possible the selloff could continue for a while, but it’s also possible that the market will stabilize on good news or simply on no more bad news. The current sell off may be the result of a confluence of factors (worsening geopolitical conflicts and moderating rate cut expectations) finally sticking to what for months has been a Teflon market. The S&P 500 largely shrugged off moderating rate cut expectations until this month. With 2024 S&P 500 earnings estimates of roughly $243 per share and a level of 5,254.35 on March 28, the forward P/E ratio of the S&P 500 index was roughly 21.62 times earnings. The historical P/E ratio of the S&P 500 is typically around 18x – 22x earnings, which means the P/E ratio at the most recent market peak was at the high end of that range. Additionally, that is based on forward estimates of earnings which are not a sure thing. If we look at the earnings reported in the last 12 months, the trailing P/E ratio of the S&P 500 is close to 25 times earnings. It may simply be that stocks were priced richly due to lofty expectations and that some disappointment has led to a repricing of stocks more in line with adjusted expectations. It may be that the equilibrium hasn’t been reached yet and that adjustment will continue. It could also be the case that Core PCE shows continued disinflation at the next release, that earnings continue to show a healthy corporate landscape, or some other good news turns the tide, and the market rallies on good news. Earnings beating expectations will bring the trailing P/E ratio down as well. To be clear, P/E ratio is not predictive of short term market trajectory and cannot be relied on as a sole indicator for investing decisions. There are always many moving parts on any given day or week in the markets and attempting to predict what those factors will be and how they will move a volatile market is often a losing proposition. This is why we collaborate with our clients to develop long-term investment strategies appropriate for their unique needs and preferences and why we counsel patience and persistence. While the market has given back much of the year-to-date gains, we can always zoom out. Since the October 27 low of the pullback last year the S&P 500 is up almost 21%, from the beginning of 2022 it’s up over 4% and from the beginning of 2020 it’s up almost 54%. We may not know what the news will bring tomorrow, but we will strive to keep you informed as the year develops.

Disclosures This communication may include forward-looking statements. All statements other than statements of historical fact are forward-looking statements (including words such as “believe,” “estimate,” “anticipate,” “may,” “will,” “should,” and “expect”). Although we believe that the expectations reflected in such forward-looking statements are reasonable, we can give no assurance that such expectations will prove to be correct. Various factors could cause actual results or performance to differ materially from those discussed in such forward-looking statements. Past performance is not indicative of any specific investment or future results. Views regarding the economy, securities markets or other specialized areas, like all predictors of future events, cannot be guaranteed to be accurate and may result in economic loss to the investor. Any information provided by H&R regarding historical market performance is for illustrative and education purposes only. Clients or prospective clients should not assume that their performance will equal or exceed historical market results and/or averages. The material listed in this communication is current as of the date noted, and is for informational purposes only, and does not contend to address the financial objectives, situation, or specific needs of any individual investor. Any information is for illustrative purposes only, and is not intended to serve as investment advice since the availability and effectiveness of any strategy is dependent upon your individual facts and circumstances. Results will vary, and no suggestion is made about how any specific solution or strategy performed in reality. Unless specifically stated to the contrary, H&R does not endorse the statements, services or performance of any third-party vendor or investment manager. Investments in securities are not insured, protected or guaranteed and may result in loss of income and/ or principal. A long-term investment approach cannot guarantee a profit.