The Basics: A Refresher on Health Savings Accounts

Let’s start with a quick review of HSA rules. An HSA is a tax-advantaged savings account which allows a taxpayer to pay for current or future medical expenses with tax-free funds. In fact, HSAs have a triple tax advantage. Much like a Traditional 401(k) or IRA, money contributed to an HSA is deductible from current income (1) and grows tax deferred (2). However, HSAs allow tax-free withdrawals (3) on the back end, like Roth accounts do, so long as those withdrawals are used for qualified medical expenses. Those qualified withdrawals don’t require the HSA owner to be a particular age, so withdrawals can occur before retirement age without penalty. This doesn’t mean there are no penalties at all. If a non-qualified withdrawal is made prior to age 65, the withdrawal is subject to ordinary income tax plus a 20% early withdrawal penalty. If an HSA owner needs to take withdrawals from an HSA after age 65 for something other than qualified medical expenses (i.e., a non-qualified withdrawal), then the withdrawal is subject to ordinary income tax, but there is no penalty. If you keep diligent records, though, you may not ever need to make a non-qualified withdrawal. This will be covered in more detail below.

To be eligible to contribute to a Health Savings Account, the IRS specifies that an individual must be covered under a High-Deductible Health Plan (HDHP). The IRS defines a HDHP as one that has a minimum annual deductible of $1,500 for self-only coverage or $3,000 for family coverage in 2023. That individual also must not have any other health coverage, including Medicare. There are certain limited exceptions to this rule which are outside of the scope of this article, but which can be found in IRS Publication 969. One important rule to note is that an individual’s spouse MAY have non-HDHP coverage, so long as that coverage does not cover the HSA-eligible individual. For instance, this means that one spouse may have non-HDHP health coverage for the family while the other may have self-only HDHP coverage and contribute to an HSA. It is also important to note that coverage under certain other healthcare reimbursement accounts such as Flexible Spending Accounts (FSAs) and Health Reimbursement Accounts (HRAs) may make an individual ineligible to contribute to an HSA.

It’s important to understand your coverage to ensure you are eligible to contribute to an HSA. If your plan is available through your employer, the employer will likely make it clear whether a healthcare plan is considered a HDHP and is eligible for an HSA. Check with your benefits department if you have questions about your coverage. Furthermore, your employer may also offer an HSA and allow you to contribute to the HSA through payroll deductions (more on this in a moment). However, an individual can open and fund an HSA without the health coverage or HSA being offered through their employer. Now that we have covered HSA basics and eligibility, let’s review contribution rules.

Health Savings Account Contribution Limits and Deadlines

Just like IRAs and 401(k)s, there is a limit to how much you can contribute to an HSA each year. For the 2023 tax year, the limits are $3,850 if you have self-only HDHP coverage and $7,750 if you have family HDHP coverage. For individuals over the age of 55, there is a catch-up provision which, in 2023, increases the contribution limit by $1,000 per HSA-eligible individual (e.g., $1,000 for self-only HDHP coverage, $2,000 for spouses with family coverage).

Like IRAs, a taxpayer typically has up until the tax filing deadline to contribute to an HSA. For tax year 2023, the tax filing deadline is April 15, 2024. However, many HSA-eligible taxpayers make contributions to their HSA through payroll deduction which will typically mean that December 31is the last contribution made to the account. If an HSA owner finds themselves wanting to make additional contributions after the end of the year and prior to the tax filing deadline, they can check with the HSA provider to determine if they can make direct contributions outside of payroll deductions or if they can specify tax year through payroll deductions. Here it is worth noting that it may be preferable to make contributions via payroll deductions. This is because pre-tax payroll deductions for HSA contributions are contributed without being subject to FICA taxes. If instead an individual makes a direct HSA contribution after having received payroll, they can deduct that contribution amount from federal taxable income, but FICA taxes will have already been paid. In short, payroll deduction contributions are the only way to contribute to an HSA pre-FICA tax.

One last point about contribution limits is that there are several ways a married couple may elect health coverage. Each spouse may have self-only HDHP coverage, or both may have family HDHP coverage, or one may have one of the above while the other has self-and-children coverage. There are additional combinations of these coverages. While I won’t list them all out, they do have planning implications and should be discussed with the benefits department, a financial advisor, a tax advisor, or all the above.

HSA Financial Planning Considerations

That brings us to special financial planning considerations regarding HSAs. As you may have already gathered, HSAs can be powerful planning tools for healthcare and retirement planning. We’ll look at a few important highlights.

One of the major benefits of an HSA is the special tax treatment of these funds. Tax-deductible contributions (including avoidance of FICA tax when contributed via payroll deductions), tax-deferred growth, and the potential for tax-free distributions in the future, can add up to significant tax savings for HSA owners. As mentioned above, it is also possible to withdraw from an HSA after age 65 without using the funds for medical expenses and without paying a penalty. This essentially makes the HSA act somewhat like a traditional IRA after age 65, except that HSAs are not subject to required minimum distributions (RMDs). This means that HSA balances can supplement retirement income if not used for medical expenses but can be left to grow tax deferred indefinitely for those fortunate enough to not need the funds.

Perhaps the most valuable fact about HSAs is that there may not ever be a need to make a non-qualified withdrawal from an HSA and face the resulting tax penalty. The reason for this is that there is no deadline to claim medical expenses. For individuals with the ability to pay for medical expenses out of pocket, they can leave their HSA untouched to grow tax-deferred, keep diligent records of “unclaimed” medical expenses and use these expenses later to take qualified, tax-free withdrawals. A medical expense is “unclaimed” if it is incurred while covered under an HDHP and paid for out-of-pocket (i.e., not yet “claimed” to make a qualified distribution from an HSA). The bottom line is to keep good records and save your receipts!

One last planning feature to discuss is the benefit available to the whole family. Under certain circumstances, a non-dependent child not older than 26 may be able to qualify to open their own HSA under their parents’ HDHP coverage and contribute up to the family maximum limit ($7,750 in 2023). In addition, the rules state that anyone can fund an eligible individual’s HSA. So, parents could fund their non-dependent child’s HSA for them. This could be a great financial head start for those with the resources to do so. There are a lot of caveats to be aware of with this strategy though. There are several rules about what constitutes a dependent and could potentially make a child ineligible to open and fund an HSA. If parents did fund an HSA for their non-dependent child, this is not deductible to the parent and would, in fact, be considered a gift and subject to gift tax rules.

With any financial planning it’s important to consult financial and tax advisors before taking action to ensure all the rules are followed appropriately.

Investing Your HSA Balance

This brings us to the last point of this article. An HSA is a useful tool for saving for future medical expenses and is in many ways a type of retirement savings account. According to the Devenir Research report 2023 Midyear HSA Market Statistics & Trends Executive Summary, only “35% of all HSA assets are in investments as of June 30th, 2023.” While HSA assets can be used for current medical expenses, investors saving those assets for retirement may want to take advantage of tax-deferred growth and see those assets increase in value over time. The percent of HSA assets invested is up from 31% a year before, so progress is being made, but a significant majority of HSA owners still aren’t taking advantage of all the benefits an HSA offers. After all, at least one of the goals with an HSA is to take tax-free withdrawals at some point in the future. As with IRA and 401(k) balances, HSA balances can be invested for long-term growth.

Most HSA providers offer a lineup of mutual funds for investment once the HSA balance reaches a certain threshold. This will be like investment offerings you may be familiar with through employer-sponsored retirement plans such as 401(k) plans. There is also an emerging trend among a few major HSA providers of offering brokerage accounts within the employer-sponsored HSA plan. This means the universe of available investments for HSA funds is expanding. It may even be possible to have in-plan HSA assets professionally managed in certain circumstances. It is important to consider your own plans with HSA balances before selecting an investment approach.

In Summary

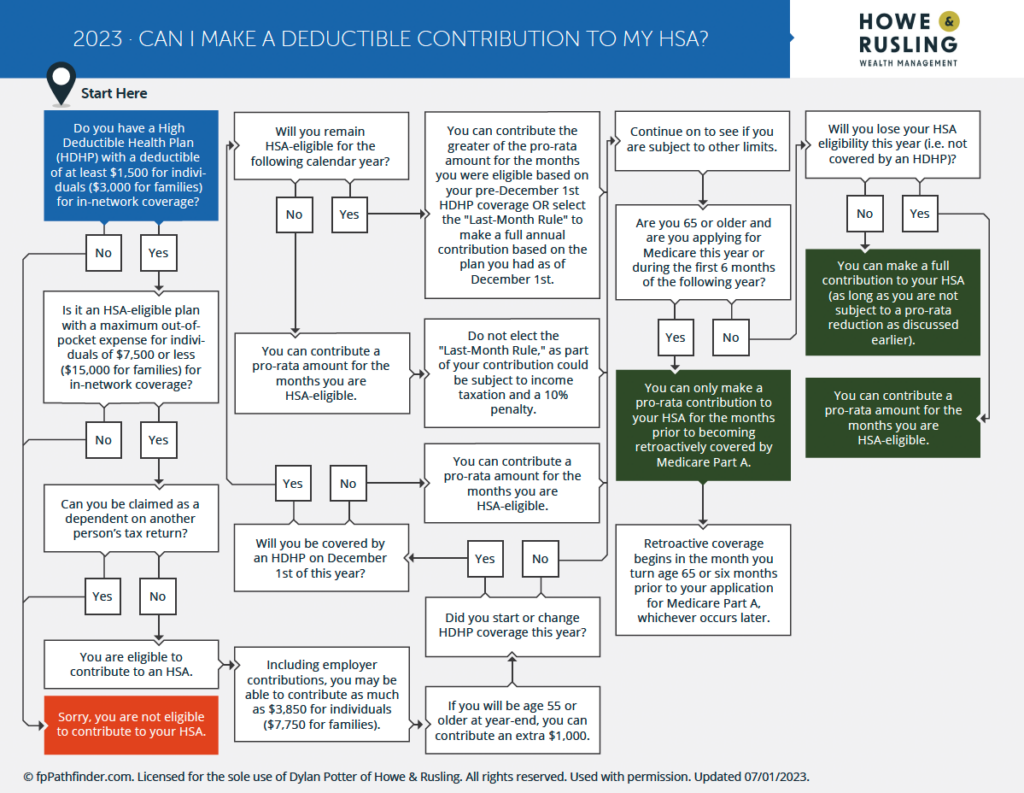

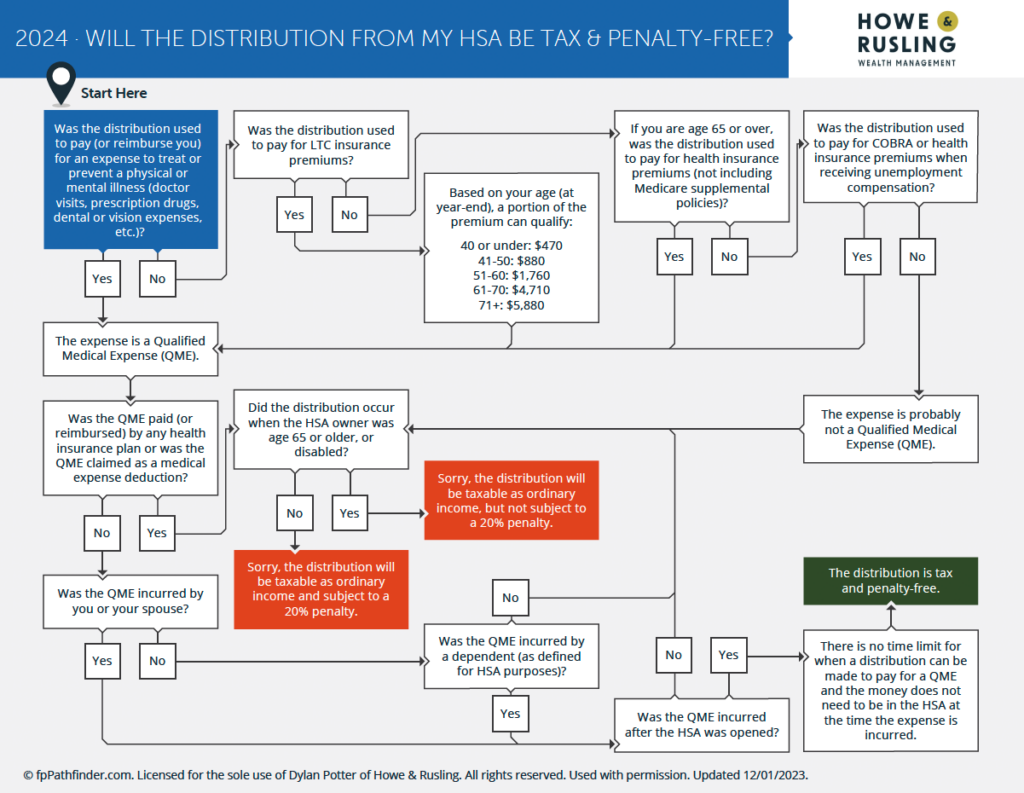

Hopefully this has given our readers a better understanding of how HSAs work and the value they can add to retirement and general financial planning. Individuals who are eligible may contribute to an HSA up to annual limits, can invest those balances for growth and may even have some useful tools in their financial plan toolkit. These rules can be complicated, so we have included a couple of flowcharts below to help you understand contribution eligibility and qualified withdrawals. As always, if you have any questions about your personal circumstances, please contact us. We are here to help.

Disclosures: Tax codes are current as of the date published and are subject to change without prior notice. A professional designation, certification, degree, or license, membership in any professional organization, or any amount of prior experience or success, should be construed by a client or prospective client as a guarantee that the client will experience a certain level of results if the investment professional or the investment professional’s firm is engaged, or continues to be engaged, to provide investment advisory services. No professional designation should be construed as an endorsement by any past or current client of the investment professional or the investment professional’s firm. A long-term investment approach cannot guarantee a profit. While H&R believes the outside data sources cited to be credible, it has not independently verified the correctness of any of their inputs or calculations and, therefore, does not warranty the accuracy of any third-party sources or information. This communication may include opinions and forward-looking statements. All statements other than statements of historical fact are opinions and/ or forward-looking statements (including words such as “believe,” “estimate,” “anticipate,” “may,” “will,” “should,” and “expect”). Although we believe that the beliefs and expectations reflected in such forward-looking statements are reasonable, we can give no assurance that such beliefs and expectations will prove to be correct. Various factors could cause actual results or performance to differ materially from those discussed in such forward-looking statements. All expressions of opinion are subject to change. You are cautioned not to place undue reliance on these forward-looking statements. Any dated information is published as of its date only. Dated and forward- looking statements speak only as of the date on which they are made. We undertake no obligation to update publicly or revise any dated or forward-looking statements.