“Let me be clear on one point: I can’t predict the short-term movements of the stock market. I haven’t the faintest idea as to whether stocks will be higher or lower a month or a year from now. What is likely, however, is that the market will move higher, perhaps substantially so, well before either sentiment or the economy turns up. So, if you wait for the robins, spring will be over.”

Warren Buffett in the Fall of 2008

This quote from one of the most well-respected investors of our time sounds so clear and straightforward, but why do we get the nearly irresistible urge to do the exact opposite with our own portfolio? The one-word answer is psychology or, more accurately, neurophysics. This newsletter will try to serve up a more complete and data-driven answer in digestible bites. First though, I’ll borrow just a few more words from the eloquent Mr. Buffett. “Be fearful when others are greedy and greedy when others are fearful.” Below is a perfect illustration of what he is referring to and a wonderful representation of how our emotions betray us as investors.

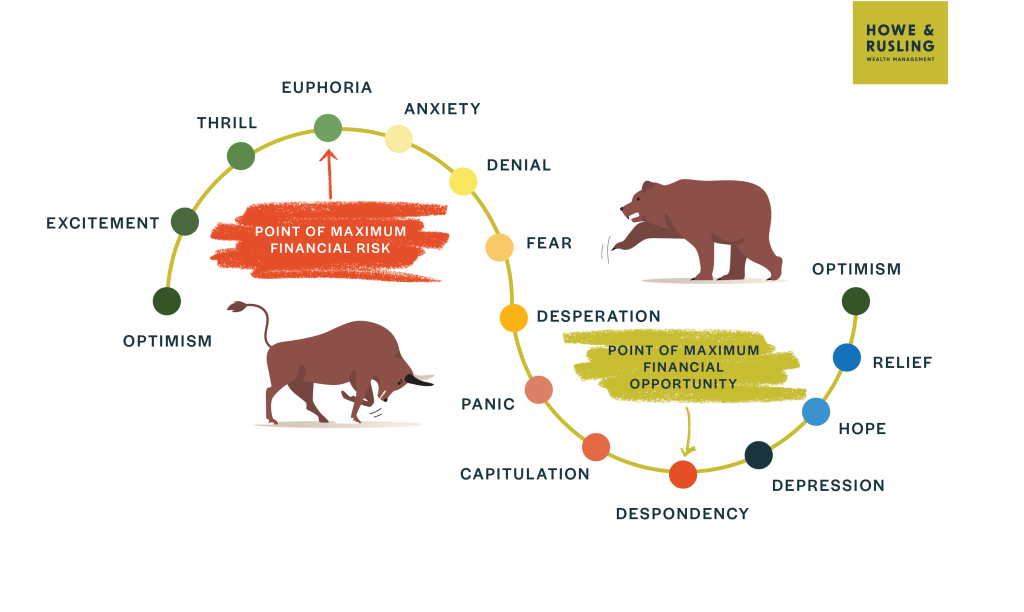

The Cycle of Market Emotions

The market cycle has 4 phases: expansion (moving up), peak (the top), contraction (moving down) and trough (the bottom).

This cycle has played on repeat for as long as there have been public investment markets. We are currently in a contraction and experiencing all the painful emotions that it brings. I agree with Mr. Buffett that no one can call the bottom of the market today. Perhaps it was last week, but we won’t know until much later with the benefit of hindsight.

Now that we know where we are on this chart, let’s define one other thing. We could say that the time “when others are greedy” refers to the optimism, excitement, thrill, and euphoria section of this illustration and “when others are fearful” goes along with desperation, panic, capitulation, and despondency. The part of the market cycle which gives us the most satisfying and powerful positive emotions comes at the point of greatest risk! It leads us to risk more, buy at a high price and believe the market cycle won’t happen this time like it always has before. And all those terrible, horrible, no good, very bad emotions come at the time when the market has the greatest opportunity to offer. However, the emotions lead us to hunker down and take risk off the table, sell at any (low) price, and believe the market cycle won’t happen this time like it always has before. Investors want to buy low and sell high, but emotions can lead to the opposite outcome.

I do not claim to be above this impulse. Very few humans are and it’s because our physiology makes this happen. You aren’t silly or foolish to feel this way, you’re perfectly normal. Stopping the fear reaction in a market contraction is about as likely as suppressing a flinch response at a jump scare in a horror film. However, just because we have an involuntary response does not mean that we then let that reaction force us to our feet and all the way out of the theater. Understanding the response can help us manage our conscious course of action in the wake of the involuntary emotional response. So, let’s examine these emotional responses and attempt to master them.

Two Brains?

Here I’ll borrow some information from the book Your Money and Your Brain by Jason Zweig. The subject matter is technical, but I will try to keep it as simple as possible. Your brain helps you navigate the world in a couple of ways. One is through fast, reflexive responses requiring no conscious thought, like pulling your hand away from a hot stove. The other is through slow, reflective responses like solving a math problem. Quick! Which line is longer?

You “know” they are the same length, but there was a part of your mind that wanted to immediately respond “the top one of course”. This is the battle between your quick reflexive brain and your slower reflective brain. Have you ever recoiled at the sight of a snake only to take a closer look and realize it’s a harmless stick? Your reflexive brain saved you from the snake and a potentially deadly bite if it was right. However, your slower reflective brain eventually assessed the situation and let you know it was safe to continue walking. Feeling silly for jumping away from a stick is a small price to pay if it helps you avoid a snake bite even just once. Both serve a purpose. Unfortunately, the reflexive brain responds to financial scenarios just as it does to a hot stove or serpentine stick. More unfortunately, it isn’t a very useful tool for making strategic investment decisions and the cost of giving into reflexive impulses for financial decisions is potentially much greater than a little embarrassment.

The Science Part

Some readers may find the science behind this fascinating while others will feel their eyes go out of focus. I’ll provide the science terms for those who crave it. It’s okay to skip this part if it doesn’t interest you, but I encourage you to bear with me.

So, why the two types of processing? Simply put, different parts of our brain are involved. Reflexive processing occurs primarily in the basal ganglia and limbic system. These are areas of the brain that process sensory stimulus below the level of conscious awareness and “light up” when something requires our attention like hazards (snake!?). This processing happens in fractions of a second and it is an incredibly efficient way of dealing with most of the stimulus we are bombarded with daily. Reflective processing occurs primarily in the prefrontal cortex and requires a lot of effort and energy. Our brains account for about 2% of our body weight but use about 20% of our caloric intake. Because of this, we efficiently use our reflexive brain for most data processing throughout a given day.

Neurochemicals in our brain also play a role. Dopamine is a primary neurotransmitter in our brain. It’s one of our reward centers. Eating a high-fat ice cream cone releases a burst of dopamine to reward us and keep us seeking out calories. Interestingly, when we get an expected outcome such as investment returns in line with expectations, we get no special dopamine kick. It’s business as usual. Not receiving the expected outcome shuts off dopamine and that doesn’t leave us with a very good feeling. Even more than a simple lack of feel-good dopamine, investment losses fire up the fear center of the brain.

When something frightening happens (snake!?) our amygdala lights up and screams at the reflective brain “do something!”. This is useful because it brings our attention to potential threats in our environment. This fear response is still present when processing more complex hazards like financial losses. The problem for investors is that this fear response typically sets in at a point in the market cycle that causes investors to sell low (after significant losses have already occurred). Once an investor has sold out, that fear leaves an impression on the brain. Once you’ve burned yourself on a hot stove, you don’t forget that the stove can burn you. In financial terms, this means that investors who sell out tend to be reluctant to reinvest and therefore miss a recovery. Eventually though, everyone else is experiencing excitement, thrill and euphoria and the reluctant investor gives in, buys high at the point of maximum risk, and gets burned all over again. The reflexive brain wants to sell low and buy high. In short, it’s a poor investor.

The Finance Part

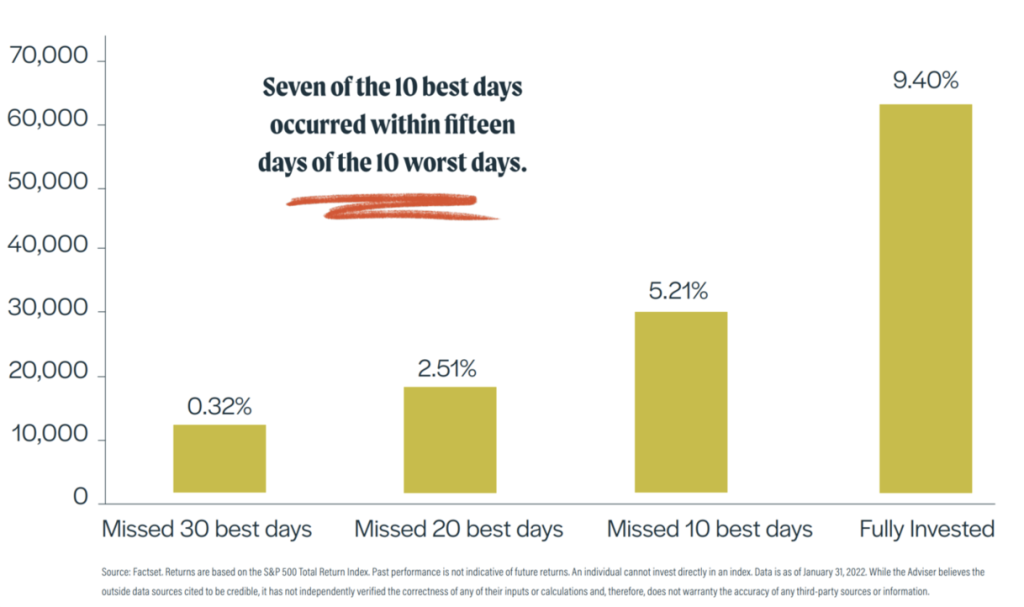

The chart below shows the cost of being out of the market on even just a handful of the best days of returns. This should look familiar because Sarah referenced the same chart in last week’s newsletter. I reference it again and will show a few additional charts to illustrate some points she made. To go back to Warren Buffett’s statement “if you wait for the robins, spring will be over”, this is the point. Some of the best days occur shortly after the worst. Even when the market seems dismal, the most effective strategy for a long-term investor is to remain in the market and take advantage of those best days when they come. It is likely it will happen before anyone knows it is happening. Once they’ve come and gone it’s a missed opportunity.

Annualized Performance of a $10,000 Investment between January 2002 & January 2022 ($)

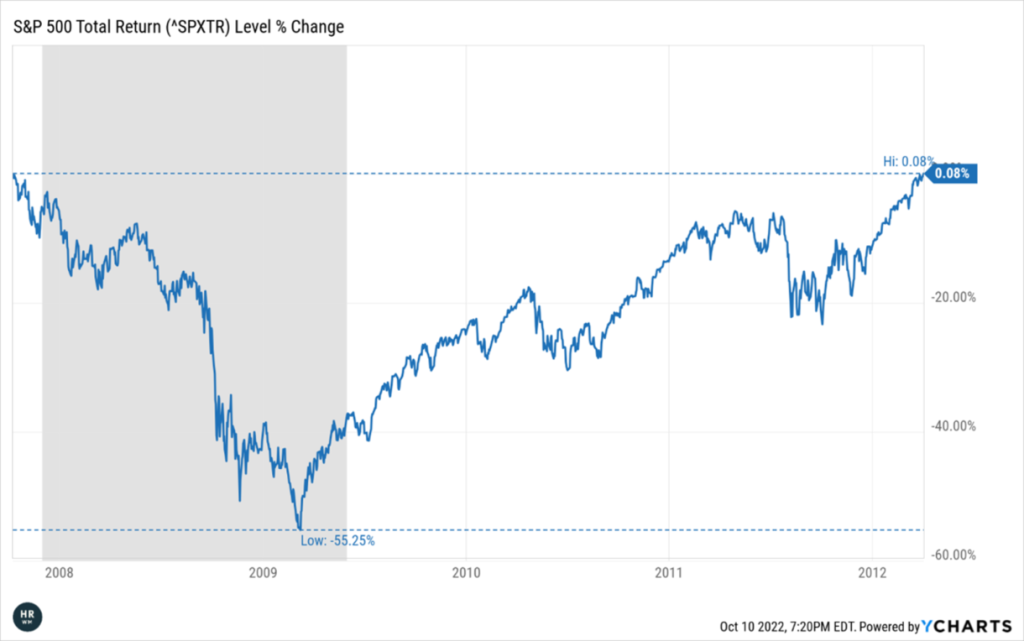

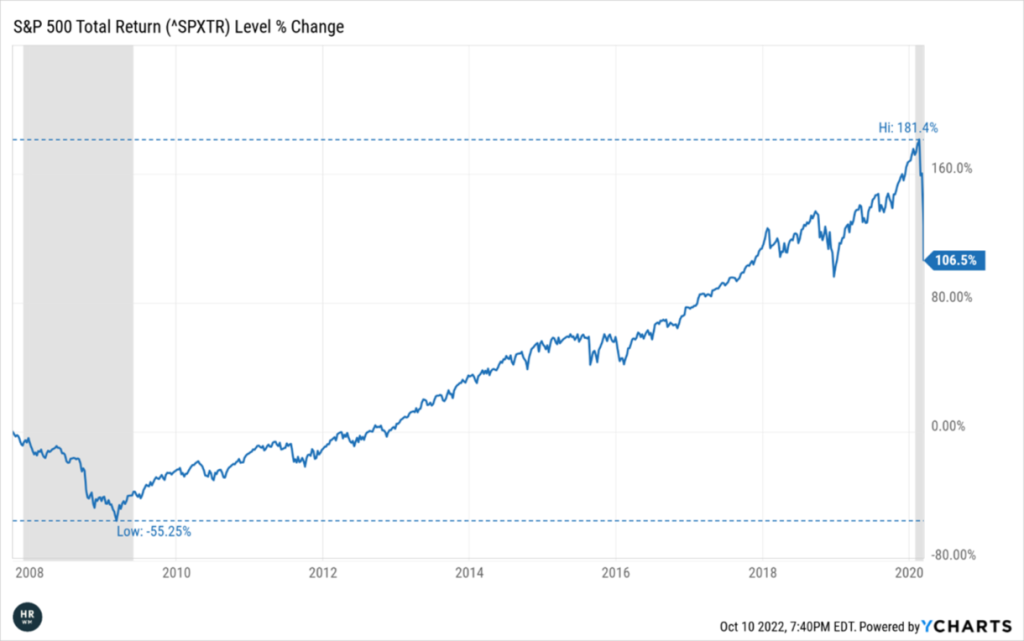

I’ll end this on a look back to a past recession to show a real-world example. The below chart shows the S&P 500 Total Return Index performance and the recession (shaded in grey) that occurred during the Global Financial Crisis. The chart begins on October 9, 2007, which was an all-time high of 2,447.03. The index then reached its bear market low on March 9, 2009, falling 55.25% over just 5 months. Note that the market began to fall before the recession officially began and the recovery began before the end of the recession. The recovery also began before the end of the recession in 2020. The chart ends on April 2, 2012, at a new high of 2,449.08. The index then went on to fall again and make another new high by year end 2012 and this pattern repeated many times during the longest bull run in US stock market history.

There is a cognitive bias called “anchoring” in which we subconsciously get stuck on a particular data point and use that “anchor point” to interpret other data. Often in a market downturn that anchor is the prior peak. However, if we shift that reference point to a couple other points, that data looks wildly different.

The record-setting bull run was broken almost exactly 11 years after the 2009 low on March 12, 2020, when the S&P 500 TR Index officially entered a new bear market. Even then the value was up 106.5% from the high of October 9, 2007. The value had doubled despite the recent losses. Notice in the chart below how many significant market declines occurred during this period.

As of close of market on 10/20/2022 the index was still up 218.2% from that 2007 high despite the recent declines, the 2020 recession, and the Global Financial Crisis that occurred in the intervening period.

Of course, past performance is not a guarantee of future performance. Every recession and bear market results from different economic drivers. However, we do know that the market has a cycle.

In Conclusion

To sum it all up, we can’t help but feel the emotions of the market cycle. It’s a part of being human to feel those emotions and you are neither wrong nor foolish to feel them. However, those emotions can steer us in the wrong direction when we let them drive investment decisions. The market cycle repeats, and nobody can predict when the seasons will change. However, we can make observations and recent history proves the truth of the opening quote. Markets often lead the economy, and a market recovery may happen before the actual economic shifts occur. Being out of the market when the pivot happens can severely hinder long-term portfolio performance. Although these bear markets are certainly painful to live through, investors who weather the storm have historically been rewarded when compared to investors who try to time the market.

I work with many people who are retired or planning to retire soon, and I often hear the understandable concern that they are not in their 30s or 40s and they don’t have time to wait for a recovery this time. It’s true that a retiree doesn’t get to benefit from dollar cost averaging in new purchases anymore. However, retirement is a long game. Your retirement date is not the finish line, it’s the starting line for your retirement plan. A well-defined financial plan, thoughtful investment approach, careful monitoring, and a not-insignificant amount of grit go a long way. When making changes to an investment plan it’s important to think in big picture terms, reflect, and adjust thoughtfully. If you haven’t already read last week’s update article from Sarah Swan, I encourage you to read it as it goes into more detail on what Howe & Rusling does to position our clients’ portfolios. You aren’t on this journey alone! We’re here to help. Remember that winter won’t last forever.